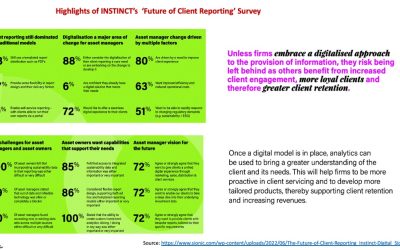

The Problem –

What is the portfolio risk if Yield Curve shifts by 1bp?

What are the CS01/DV01/KRD’s of the portfolio?

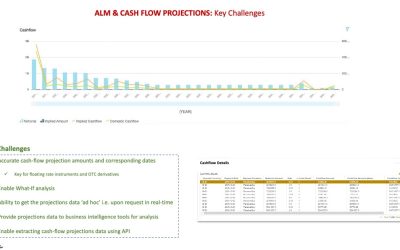

What are the projected cash flows of the portfolio?

How much will we lose/gain if we have a 2007 like crash again?

What is my exposure to a specific country/sector/asset class?

What is the manager’s value add?

How is the portfolio doing compared to the policy index?

.

.

.

A good ‘Portfolio Insights’ solution not only provides the ability to present the necessary analytics but also helps answer some of the ‘What-If’ questions to get a deeper analysis for Risk/Portfolio manager.

Key analytics necessary for answering above includes the ones mentioned last week – See https://bit.ly/3d4WXms

In addition for ‘Fixed Income’ portfolios some of key analytics needed for deep actionable insights are –

– Sensitivity Analysis: DV01/CS01/KRD, etc

– Security Analytics: Duration, Convexity, Yield to maturity, etc.

– Cashflow Projections: Income and Maturity Amounts by date/security and aggregated amounts by date.

– Fixed Income Attribution: With yield curve and duration effects

As before a next level analysis of the portfolio will interpret basics using NLP leaving the complex ones to the manager.