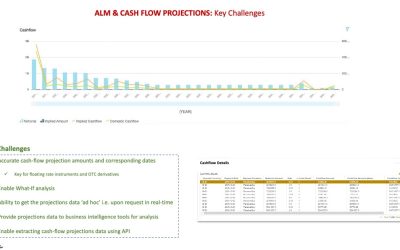

PROBLEM

Need for Liquidity Risk model for multi-asset portfolios that is simpler to use and easier to understand for regulators and savvy investors

CHALLENGE

– Market data for volumes of listed securities and assumptions around liquidity days for illiquid assets

– Ability to run real-time liquidity analysis

SOLUTION

An approach to a simpler liquidity risk model involves using numerical iteration using holdings data, security exposures, traded volume (for listed securities) and realistic assumptions around liquidity days for non-listed securities.

‘Volume Participation Rate’ and ‘%Fund Redeemed’ can be the key configurable parameters for the calculations.

‘Portfolio Liquidity Profile’ and ‘Liquidity Scenario Details’ at both the portfolio and security level will be key outputs from the analysis.

SO WHAT?

For the Portfolio Manager, performing above liquidity analysis in real-time by tuning input parameters using ‘What-If ‘ (add/change position) will ensure liquidity risk requirement is per the portfolio’s IP mandate.

From an Investor perspective providing the above results in BI dashboard and/or reports will provide the necessary comfort in knowing that the portfolio can handle stress events.