THE PROBLEM

What are the key forward looking risk measures necessary to perform effective risk analysis on a multi-asset portfolio?

THE APPROACH

In the last 3 posts, we covered Holdings view, Ex-Post and VaR Detail. In this last post under this category, our focus will be on getting details on key Security & Portfolio Analytics necessary for further analysis.

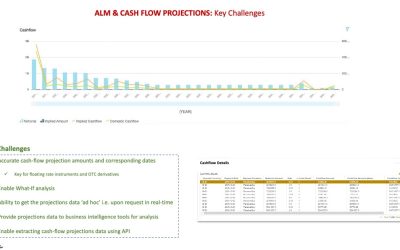

Cash flow Projections

At both the security and portfolio level, the projected cash flows by currency helps understand the timing of the flows and better manage the funding/trading liquidity risks of portfolios containing income-producing securities

Economic Value of Equity (EvE)

Shocked value of portfolio for key risk factor shock scenarios

Earnings At Risk (EaR)

Change in portfolio cash flows for key interest rate shock scenarios affecting float rate instruments

Key Rate Duration (KRD)

Changes in price/value when there are non-parallel shifts in the yield curve across all maturities.

Other Analytics

For portfolio construction, optimization and/or hedging some of the key analytics necessary for analysis include – Bond Yield (YTM), DV01, Convexity, ZSpread, Macaulay/Modified/Effective Duration, Continuous Dividend Yield, Implied Volatility, Option Adjusted Spread (OAS) and Option Greeks(Delta, Vega, Gamma, Theta, Volga and Rho)

HOW TO?

As has been the key theme through the posts related to real-time risk analysis – the need for bringing all of this data together into one place irrespective of the source system(s) is important for performing analysis to get real-time actionable insights.

Integrating systems using modern ‘cloud’ technology, i.e. microservices architecture that can scale dynamically depending on data volume, is paramount for this to be successful.

Implementing above will enable firms to operate in scale using the ‘Pay Per Use’ business model, where expenses do not scale linearly as portfolio volumes grow – a key competitive differentiator for the firm to position for the long-term.