On Dec 10, 2021 the Fed in a letter to the banks mentioned that lenders must maintain sufficient margin when dealing with investment funds and they need to be responsible for understanding their positions.

Key takeaways from the Fed for firms managing multi-asset portfolio, specifically large derivative positions

1. Receive adequate information with appropriate frequency to understand the risks of the investment fund, including position and counterparty concentrations, and either reconsider the relationship or set sufficiently conservative terms for the relationship if the client does not meet appropriate levels of transparency;

2. Ensure the risk-management and governance approach applied to the investment fund is capable of identifying the fund’s risk initially and monitoring it throughout the relationship, and ensure applicable areas of the firm – including the business line and the oversight function – are aware of the risk their investment fund clients pose to the firm and have tools to manage that risk; and

3. Ensure that margin practices remain appropriate to the fund’s risk profile as it evolves, avoiding inflexible and risk-insensitive margin terms or extended close-out periods with their investment fund clients.

So what does this mean for the buy-side holding derivative positions from a ‘risk’ perspective?

Although this letter was for banks holding large derivative positions, to some extent they apply to buy-side firms with large derivative positions and thus is a helpful guidance necessary to strengthen their risk management practices.

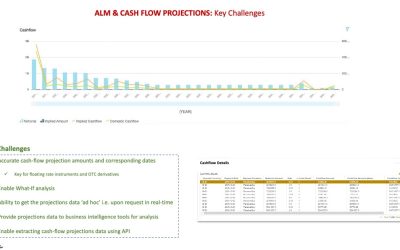

Key factors to consider for buy-side include –

1. Portfolio exposures at both the top level and by look-through

2. Monitoring risk limits and counterparty risks measures

3. Using simulation (and not parametric-approach because of portfolios holding non-linear instruments) for portfolio re-valuation to calculate forward looking risk analytics such as – VaR, Tail Risk and Stressed VaR

4. Monitoring key liquidity risk measures and

5. Perform ‘What If’ scenario analysis

The ability to perform all the above in real-time and monitoring it through a dashboard will be key to ensure firms risk management will be robust and can adapt to changing market needs.

To make the above a reality – modern architecture, using ‘cloud’ technology, i.e. microservices using API integration with existing legacy systems, will be necessary.

This, along with a cloud data warehouse, can enable dashboards with real-time insights into portfolio(s) risks, can position the firm for the future from a ‘risk management’ perspective.

See full letter here – https://bit.ly/3IPxCeu