For portfolios with relatively simpler asset mix (i.e. wealth management) – risk factor shocks such as change in interest rates, inflation expectation, volatility, FX changes, index changes, etc will be key variables that need to be shocked.

Stress results from above shocks, along with investor input on risk-appetite, will need to be used to modify portfolio composition to get the portfolio to a target risk state.

However, for complex institutional portfolios – advanced risk factors such as Credit Spread01, PV01, VaR analysis, yield curve analysis, correlation analysis, etc. along with scenarios that combine multiple such factors will become more important.

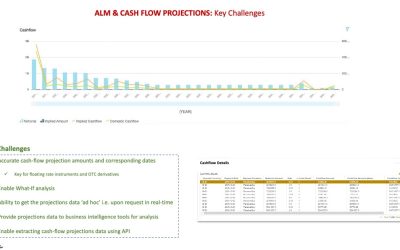

So what are some of the key challenges facing firms in carrying out such an analysis currently?

– Ability to perform risk analysis in real-time

– Ability to review potential outliers caused because of data issues (missing data or bad data), so reporting is accurate

– Assumptions around use of correct proxies for securities where data is not available

And what can firms do now to address above challenges?

– Upgrade or build RISK systems with ‘cloud’ technology framework using microservices

– Provide ability to perform real-time risk analysis by integrating existing legacy data management systems using API

– Enable ‘Pay per Use’ operating model to scale systems dynamically as volumes grow and still be performant.

– Provide Business Intelligence (BI) tools to managers to help understand risk impact in real-time in order to mitigate risk and better manage their portfolios.