THE PROBLEM

Continuing from the previous post on the need for moving away from Legacy Systems for Risk Analysis for Investment firms – In this post, the focus is from the end user perspective.

CURRENT STATE

Key advantages of legacy systems include the maturity of the core functionality and the system stability. However, this comes at an increased costs because of the need for more operational personal for support and system maintenance. Some of the other cons are :

-Lack of transparency, of the calculation details

-Data ‘push’ in batch (say of holdings data)

-Batching of risk calculations

-Additional time to set up new holding/reference data

-Batch loading of client prices: Again, a data ‘push’ for relevant asset classes if necessary

– Inability to scale calculations dynamically as volumes grow, resulting in ‘wait’ times for getting results

TARGET STATE

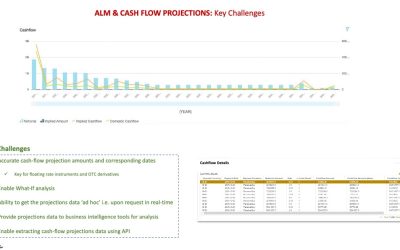

– ‘Pull’ Holdings/Price data as necessary from source systems enabling ad hoc run of calculations – eliminate need for recon between source system and risk system. In addition, this eliminates ‘batch’ processing.

– Enable calculation transparency by allowing the user to review the details of calculations along with its results when necessary – therefore reduced need for IT or system analysts for user support

– Need to perform risk analysis in real-time (not as ‘batch mode’) by risk analysts to get results for questions such as below is a growing trend:

1. How did we fare in covid crisis and the last 6 weeks (i.e. current geopolitical event) and what happens if rates move up?

– Historical stress scenario and Hypothetical Scenario analysis

2. What positions can we add/reduce to optimize portfolio risk?

– Marginal VaR, ComponentVaR

3. What is the change in portfolio risk if we add/change specific positions?

– What-If Analysis, Liquidity Risk Analysis

etc…

GETTING TO TARGET STATE

– Separate sourcing of data (holdings/prices) from the running of calculations

— Risk system should not store Holdings/Price data

— Use API to integrate between the risk and other data systems (holdings/reference/market)

– Define necessary data attributes for each instrument from the source system for which risk analytics is necessary

– Enable user interface to view calculation details when required

– Enable self-service so users can monitor calculation runs and manage data/configuration errors

– Provide capability to change configuration and run/re-run calculations in real-time

– Provide ability to push calculation results to downstream systems, including reporting and business intelligence (BI) using API technology

Modern architectures using ‘cloud’ technology can help firms get to the above target state. These firms recognize managing ‘portfolio risk’ as one of the core operational components and, therefore, will continue to have a competitive advantage in the long term.